Game, Set and Death for Memecoins?💀

Happy Sunday dispatchers!

Where are we at with them memecoins, eh? The mania that promised to mint millionaires overnight? The supercycle that was supposed to transform $1,000 into a down payment on your dream house?

Some of us clutched rare alpha like precious gems, others endured sleepless nights chasing pumps and dumps on five screens, many waited patiently for that life-changing 1000% gain that would let us tell our bosses where to shove it.

As celebrity tokens implode, political scandals erupt, and North Korean hackers launder millions through cute dog coins, a sobering question emerges: Should we even be waiting for the next memecoin wave? Or have we witnessed the final act of crypto's most chaotic sideshow?

Trade Smarter, Earn More – With Bitget Africa!

Crypto trading can be complicated. Maximising rewards while you trade? Even trickier.

Bitget Africa makes it easy with powerful tools, deep liquidity, and exclusive rewards— so you can trade with confidence.

Trade 500+ cryptocurrencies with ultra-low fees

Copy trade top investors and earn like the pros

Enjoy deep liquidity & advanced trading tools

Secure, user-friendly, and designed for all traders

Whether you're a beginner or a seasoned trader, Bitget Africa gives you the edge you need.

The best part? Get started in minutes—no complex setups, just seamless trading.

Start trading now & unlock your potential.

Last February, CryptoQuant CEO Ki Young Ju made a curious observation: "Memecoins are archetypes of the collective unconscious."

He was referencing psychiatrist Carl Jung's concept of shared symbols that underpin human culture — suggesting memecoins tap into something elemental in our nature. Animal tokens represent ancient shamanism; celebrity coins embody our worship of powerful individuals. If memecoins indeed represent our collective unconscious, then crypto's psyche is currently experiencing a profound trauma.

In a span of just 45 days, the once-vibrant memecoin market has suffered a catastrophic series of blows from which it may never recover. Presidential rug pulls, political scandals, and even North Korean hackers have conspired to drain both capital and credibility from a sector that once defined crypto's playful, freewheeling ethos.

"What crypto is digesting right now is the end of the memecoin boom," wrote Bitwise CIO Matt Hougan. "The combination of Melania, Libra, and the Lazarus Group using memecoins to launder stolen ETH will kill it dead."

How did we get here?

Get 17% discount on our annual plans and access our weekly premium features (HashedIn, Wormhole, Rabbit hole and Mempool) and subscribers only posts.

The Trump Family Token Empire

The memecoin death spiral began, ironically, at what seemed like its moment of greatest triumph.

On January 17, just days before his inauguration, president-elect Donald Trump launched his namesake token. Within 48 hours, TRUMP had rocketed 1,108%, from $6.20 to $75.35, reaching a market capitalisation of $24 billion. This briefly made it one of the 20 most valuable cryptocurrencies in the world.

Read: The On-chain President ⛓️

The First Lady quickly followed suit. Melania Trump launched her own token on January 19, and it promptly surged to a $1.6 billion market cap.

Even Trump's inauguration preacher, Reverend Lorenzo Sewell, got in on the action with his own memecoin.

The presidential endorsement seemed to validate memecoins as a legitimate asset class after years on crypto's fringes. Far from signalling mainstream acceptance, the Trump family's memecoin adventure would mark the beginning of the end.

TRUMP has since collapsed more than 83% from its all-time high, erasing about $20 billion in market value. $MELANIA fared even worse, plummeting 93% from its peak.

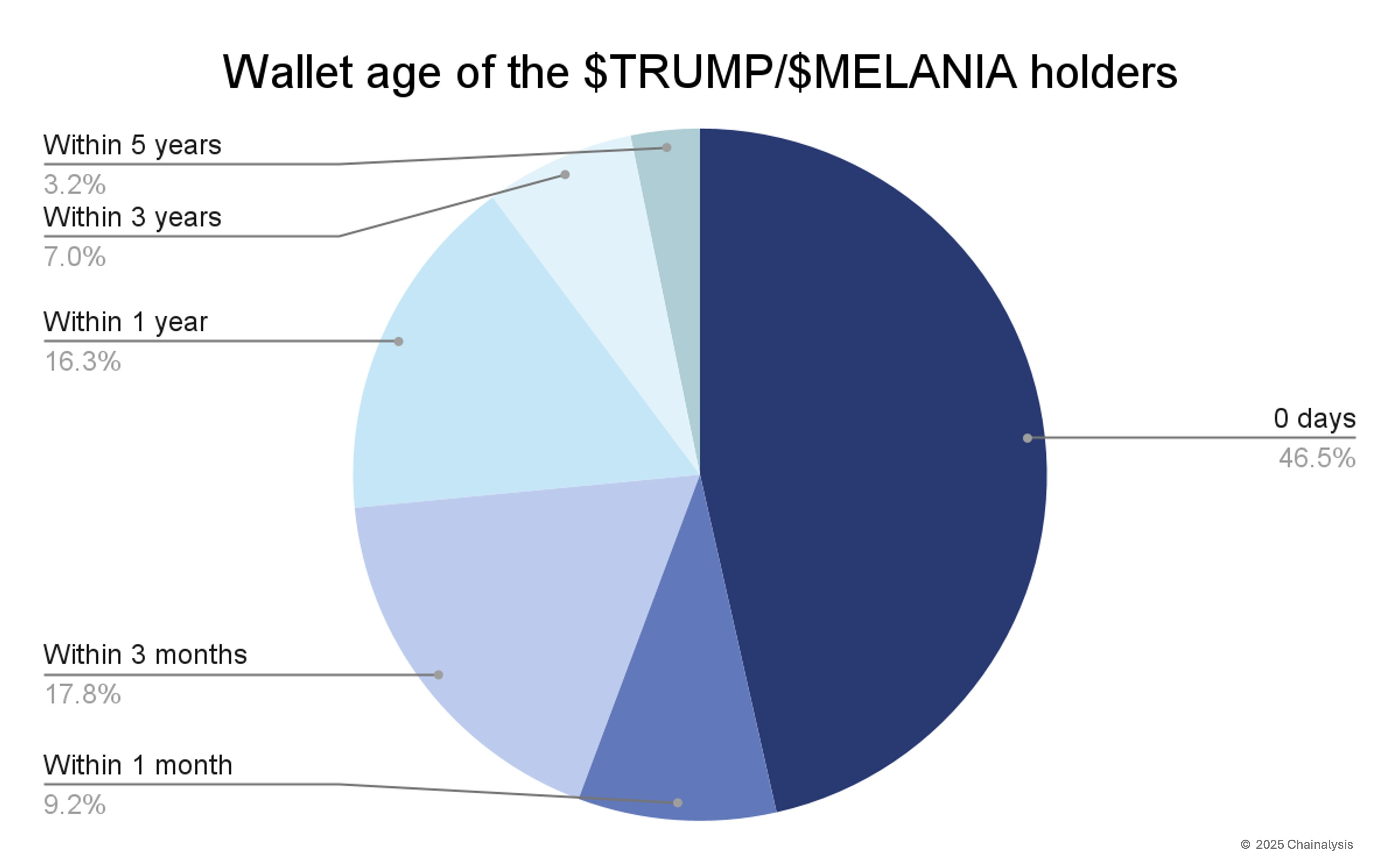

According to blockchain intelligence firm Chainalysis, roughly 50% of Trump and Melania token holders had never bought a Solana token before. Almost half created their crypto wallets the day they purchased the tokens.

This influx of inexperienced retail investors buying at the top — only to watch their investments crater — has severely damaged crypto's reputation among mainstream audiences. These weren't crypto natives who understood the risks; these were people around the world drawn in by Trump's celebrity.

The fallout has been swift. California Democrat Sam Liccardo announced the introduction of the "Modern Emoluments and Malfeasance Enforcement Act" — aka the MEME Act — which would prohibit the president, vice president, members of Congress, senior executive officials and their family members from issuing, sponsoring or endorsing digital assets.

"Almost every one of the 800,000 people that bought the memecoin lost a lot of money. We're going to ensure there are criminal and civil penalties so people can sue," Liccardo claimed.

While Trump and his family haven't actually sold their tokens (which would constitute a true "rug pull" in crypto parlance), the damage to investor confidence was already done.

The presidential token debacle was merely the opening act in the memecoin tragedy.

The Libra Scandal: Memecoin's Watergate

If the Trump token collapse was a body blow to the memecoin market, what happened next was a knockout punch.

On February 14, Argentine President Javier Milei promoted a little-known Solana token called Libra in a post on X. According to the project's pitch, Libra was designed to "fund small Argentine businesses and startups." Within hours, the token's market cap more than quadrupled to $4.5 billion.

Read: When Presidents Play With Memes 🏛️

Then everything unravelled. Milei deleted his post, and Libra's value plummeted more than 90%. Analysis by blockchain intelligence firm TRM Labs revealed that wallets associated with Libra's creators received one million tokens after launch, placed them in a liquidity pool, and then withdrew over $90 million worth of Solana and USDC — directly contributing to the token's price collapse.

According to Nansen, over 13,000 investors lost a combined $251 million in the Libra debacle. Meanwhile, just 2,101 wallets managed to profit a total of $180 million.

The political fallout was immediate. Milei now faces impeachment calls in Argentina, and a judge has been selected to investigate allegations of fraud against the president. While Milei has denied the allegations, saying he "was not aware of the details of the project," the damage to both his reputation and the broader memecoin market has been severe.

Hayden Davis, the 28-year-old Texan who helped launch both Libra and Melania Trump's token, allegedly boasted in text messages about paying Milei's sister — the president's closest adviser — to secure his endorsement.

Read: Hayden Davis: Architect of Presidential Crypto 👨🏼💻

The Libra scandal exposed what many skeptics had long suspected: the memecoin market was never the democratic, permissionless playground its proponents claimed.

"The memecoin trade was entirely based on a claim that was ultimately exposed as a lie — that the casino was at least fair. Memecoins are cooked. There will still be launches and probably some winners, but the meta is done," wrote venture capitalist Nic Carter.

A Global Political Epidemic

The Milei-Libra fiasco was far from an isolated incident. After Trump's token launch, at least five world leaders got embroiled in memecoin scandals in just a month's time.

On February 10, Central African Republic President Faustin-Archange Touadéra promoted a national token called CAR. The project's awkward launch — including a website that went dark and an X account that was suspended — created confusion about its legitimacy.

Deepfake detection tools flagged videos of Touadéra as likely AI-generated, further undermining confidence. The token's market cap plummeted from $600 million to nearly zero in two days.

On February 15, scammers impersonated Bermuda's Premier David Burt on X, using a fake account with an official-looking gray verification badge. The account promoted a "Bermuda National Coin" to followers. Burt's real account doesn't even have the verification badge that the imposters somehow obtained.

Two days later, the annual Saudi Law Conference's X account was hacked and altered to impersonate Saudi Arabia's Prime Minister, Crown Prince Mohammed bin Salman, to promote an "Official" Saudi Arabia memecoin called KSA. Despite the obvious red flags — the token was launched on Pump.fun by a developer with just two followers. The incident further contributed to the sense that memecoin mania had spiralled out of control.

Malaysia's longest-serving prime minister, Mahathir Mohamad, saw his X account hacked on February 5 to promote a MALAYSIA token.

A day after Trump's token launch, the Cuban government's X account was compromised to promote a CUBA token.

The pattern was clear: memecoin promoters were increasingly targeting political figures — whether through endorsement deals or outright impersonation — to lend legitimacy to projects that often turned out to be elaborate pump-and-dump schemes.

The North Korean Connection

Besides presidential endorsements and political scandals, the memecoin sector faced yet another crisis from an unexpected source: North Korean hackers.

On February 22, the notorious Lazarus Group was linked to a massive $1.5 billion hack of cryptocurrency exchange Bybit — the largest single hack in crypto history. Days later, blockchain sleuth ZackXBT revealed that the hackers were attempting to launder some of the stolen funds through Solana's popular memecoin platform, Pump.fun.

This revelation directly connected memecoins to one of the most sophisticated and dangerous cyber threats in the world. North Korea's regime has a documented history of using stolen crypto funds to finance its nuclear weapons program, making this association particularly toxic for the memecoin sector.

As if to underscore the point, Pump.fun's own X account was compromised on February 26 to promote a fake governance token called "PUMP" and other fraudulent coins. According to ZackXBT, this hack was directly tied to similar compromises of other prominent crypto accounts.

The cumulative effect of these incidents — presidential tokens collapsing, political scandals erupting, and North Korean hackers exploiting the memecoin ecosystem — has disrupted a sector already struggling with sustainability issues.

The Unsustainable Economics

Even without the high-profile scandals, the memecoin sector was showing clear signs of unsustainable excess by early 2025.

A November 2024 report from Binance Research found that more than 75% of all memecoins ever created were spawned in 2024 alone. Even more telling: 97% of these tokens had become completely inactive, generating no trading volume whatsoever. Just 0.23% of memecoins maintained a market cap above $1 million.

The proliferation reached absurd levels in January 2025, with over 600,000 new tokens launched in a single month — most of them memecoins. This fragmentation of capital made it increasingly difficult for any individual coin to sustain its price or achieve significant valuation.

The velocity of memecoins changing hands also highlighted their purely speculative nature. According to research from ArkStream Capital, the daily trade volume for meme tokens averaged 11% of the sector's combined market cap. By comparison, DeFi tokens saw daily turnover of 5%, Layer 2 tokens 7%, and Layer 1 network tokens just 4%.

Put simply, people weren't buying memecoins to hold them—they were buying to flip them as quickly as possible.

Memecoin listings did become an effective vehicle for centralised exchanges seeking to boost trading volume. By early 2025, memecoins accounted for a staggering 20% of the top 30 spot trading pairs by volume on Binance. This liquidity bonanza came at the expense of genuine utility and long-term value.

The Regulatory Reckoning

The SEC's Division of Corporation Finance declared on February 27 that memecoins aren't securities under federal law and therefore don't need to be registered with the Commission.

"Memecoins do not involve the offer and sale of securities under the federal securities laws," the agency stated, describing them as "akin to collectibles" that "typically have limited or no use or functionality."

This might appear to give memecoins a regulatory reprieve, but the SEC added a crucial caveat: fraudulent memecoin sales "may be subject to enforcement action or prosecution by other federal or state agencies." This clarification puts the regulatory ball in the CFTC's court.

Elizabeth Davis, partner at the law firm Davis Wright Tremaine and a former CFTC chief trial attorney, argued that the CFTC would be the right authority to oversee memecoin regulation.

Former CFTC Chair Chris Giancarlo previously blamed the SEC for the disorder in the memecoin market, while the SEC's crypto task force head, Hester Peirce, later declared that memecoins fall outside the agency's purview.

The regulatory confusion itself highlights the challenges in governing a market that evolved so rapidly that regulators couldn't keep pace.

Solana's Identity Crisis

An intriguing subplot in the memecoin saga is Solana's identity crisis.

When Anatoly Yakovenko launched Solana in 2020, his vision was to create the "Nasdaq on the blockchain", a home for sophisticated financial markets. Instead, Solana became crypto's premiere memecoin playground, with its Pump.fun launchpad facilitating the creation of 7.5 million tokens and generating over $550 million in revenue.

The memecoin boom was both a blessing and a curse for Solana. It drove infrastructure improvements and brought waves of new users to the network. It also led many serious investors to dismiss Solana as just a "memechain" rather than the high-performance financial platform it was designed to be.

Read: Raydium and Memecoin Woes Rattle Solana 🚨

Chris Chung, CEO of Titan, said the potential approval of a Solana ETF this year could be the catalyst that helps the blockchain shed its memecoin reputation.

"An ETF enhances the credibility of any crypto asset in the TradFi world. This is significant because it recognises Solana for what it was designed to be: a serious blockchain supporting large-scale trading and real-life use cases."

Correction, Not Collapse

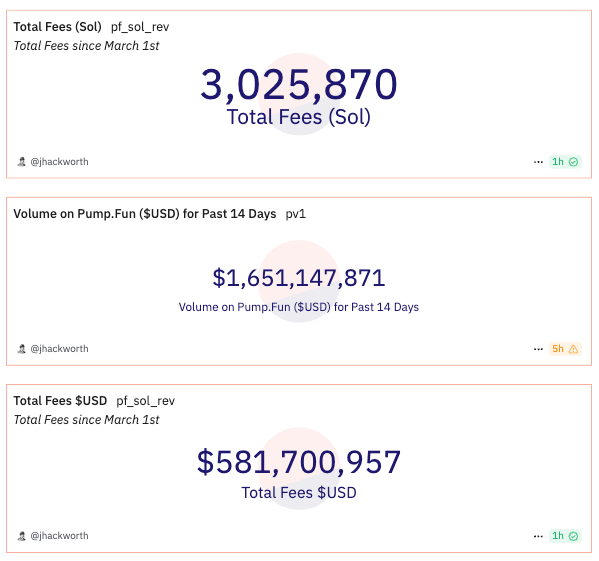

Despite the catastrophic series of scandals from presidential tokens to the Libra fiasco, declaring memecoins "dead" would be premature? Pump.Fun still generated $1.77 billion in trading volume over just two weeks in February, with over $580 million in fees since March—substantial figures that suggest a market in correction rather than collapse.

What we're witnessing is likely the end of the celebrity and political token era, not the demise of memecoins entirely. As daily volumes have dropped 80% from mid-February peaks, the market appears to be shedding its most problematic elements while potentially evolving toward more sustainable models. The wild west phase may be ending, but as with previous crypto cycles, transformation rather than extinction remains the more probable outcome.

Token Dispatch View 🔍

The memecoin market isn't dead—it's experiencing a crisis of confidence.

When politics and insider trading collided in the Libra scandal, it fractured the foundational promise of memecoins: that anyone could participate on equal footing. The collapse of trust has been swift and brutal, draining liquidity faster than North Korean hackers could launder it. An 80% volume drop doesn't lie.

Crypto rarely dies; it transforms. Each cycle purges excesses and recalibrates expectations. The current liquidity squeeze isn't limited to memecoins—it's part of a broader macro correction affecting Bitcoin, Ethereum, and everything in between.

What's truly fascinating is how quickly power players hijacked the memecoin narrative. Politicians, their families, and connected insiders twisted a grassroots phenomenon into another rigged game. The MEME Act isn't just legislative theater; it's an acknowledgment that something fundamentally changed when presidents and premiers entered the chat.

The $1.77 billion in recent trading suggests there's still a pulse, but markets run on confidence more than capital. For memecoins to truly recover, they'll need to rebuild trust in a system that briefly promised democratised access but delivered the same old power dynamics in new wrapping.

The party isn't over. But the VIPs crashing it might have ruined the vibe for good.

Week That Was 📆

Saturday: All That Troubles Ethereum 🌪️

Wednesday: Inside the $1.5B Crypto Carnage 📉

Tuesday: Case Closed: SEC’s Crypto Cleanup🧹

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. You can find all about us here 🙌

If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us.

Disclaimer: This newsletter contains sponsored content and affiliate links. All sponsored content is clearly marked. Opinions expressed by sponsors or in sponsored content are their own and do not necessarily reflect the views of this newsletter or its authors. We may receive compensation from featured products/services. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.