The Great Stablecoin Collision 🪙

Happy Sunday dispatchers!

A $5.9 trillion asset manager enters the arena.

A sparsely populated state prepares to mint its own digital dollars.

Democratic senators warn of financial collapse. And the US president watches his family-backed token face congressional scrutiny.

The stablecoin gold rush is on, and the stakes couldn't be higher.

This is about whether the dollar's global reign can be extended through blockchain, or whether this proliferation might inadvertently accelerate its decline.

"Dude, Arcium is actually wild."

You know how companies always need access to your data to "improve services"? Yeah, that’s just a fancy way of saying they collect, sell, and sometimes leak your info. Arcium flips that on its head.

It lets businesses use data without ever seeing it. Like, AI can train on encrypted data, banks can process transactions without exposing user info, and companies can collaborate on sensitive data without actually sharing it.

Basically, it’s privacy that actually works. No gimmicks, no "just trust us" nonsense.

What can this actually do?

- AI models that don’t need to see your data to learn from it

- Banks that detect fraud without snooping on your transactions

- Companies that analyze trends without selling your personal info

- Cloud computing that doesn’t need you to "trust the provider"

This isn’t some quiet tech upgrade. This changes the game. Check it out!

When we talk about stablecoins, we're no longer discussing a fringe crypto experiment.

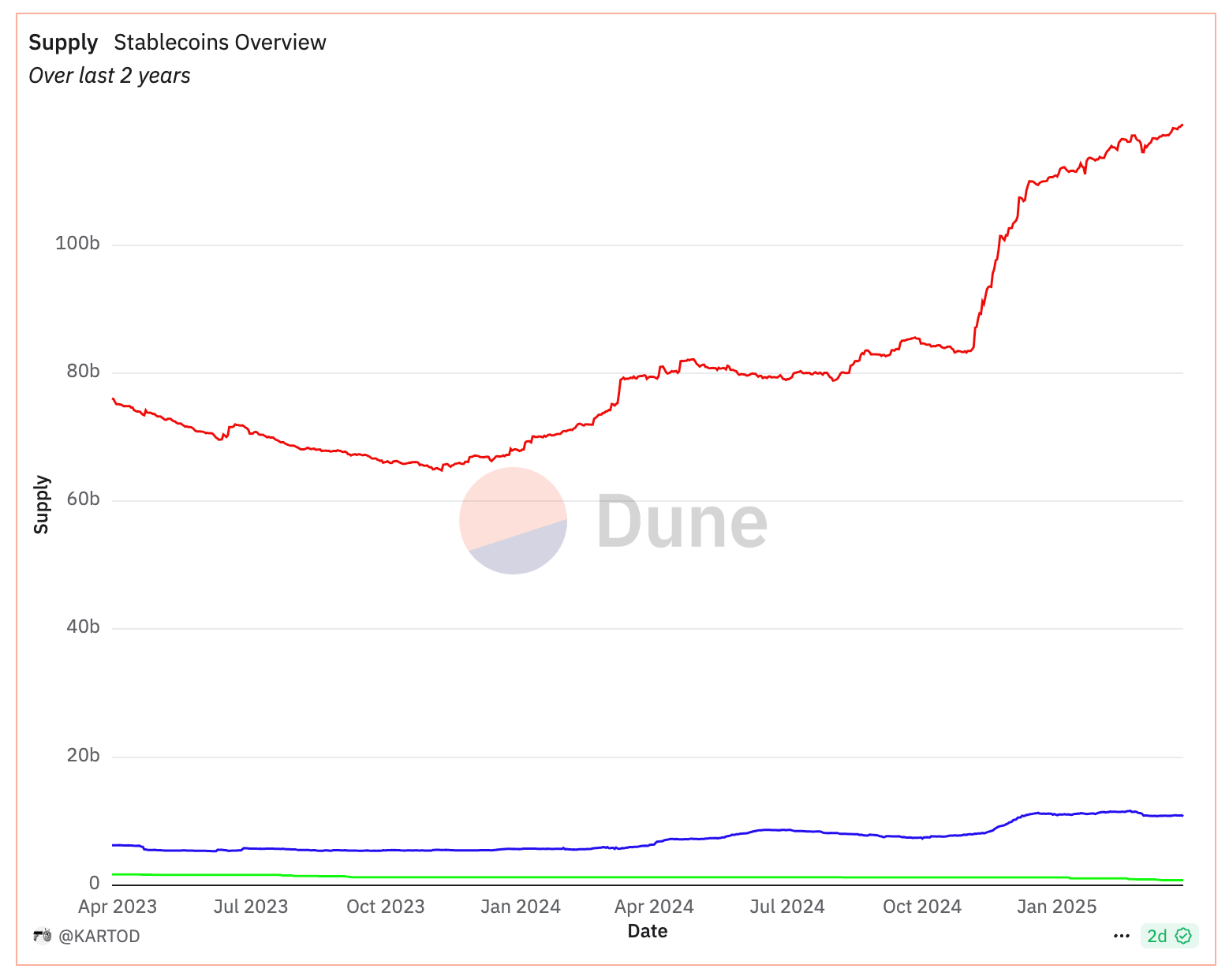

The market for these dollar-pegged tokens has swelled 53% in 2024 alone, surpassing $238 billion in circulation and facilitating a staggering $5.8 trillion in on-chain volume.

That explosive growth hasn't gone unnoticed.

In just the past week, Fidelity Investments revealed plans for its own stablecoin, Wyoming announced a July target for launching its state-backed token, Trump-affiliated World Liberty Financial debuted USD1, and Custodia Bank with Vantage Bank issued what they're calling "America's first bank-issued stablecoin on a permissionless blockchain."

We're witnessing an unprecedented rush toward digital dollars from players who, until recently, viewed crypto with suspicion or outright hostility.

And it's not just banks and asset managers.

The NYSE's parent company, Intercontinental Exchange, disclosed it's exploring USDC integration for new products. T. Rowe Price's global technology equity portfolio manager, Dominic Rizzo, called stablecoins "the most obvious use case for crypto" with "big, big potential."

Even Japan's getting involved, with Circle securing a license to operate USDC there in partnership with local heavyweight SBI Holdings.

When everyone from state governments to Wall Street giants to presidential families is fighting for position in the same market, a collision is inevitable.

And these competing visions for digital dollars couldn't be more different.

Get 17% discount on our annual plans and access our weekly premium features (HashedIn, Wormhole, Rabbit hole and Mempool) and subscribers only posts. Also, show us some love on Twitter and Telegram.

A Fragmented Future

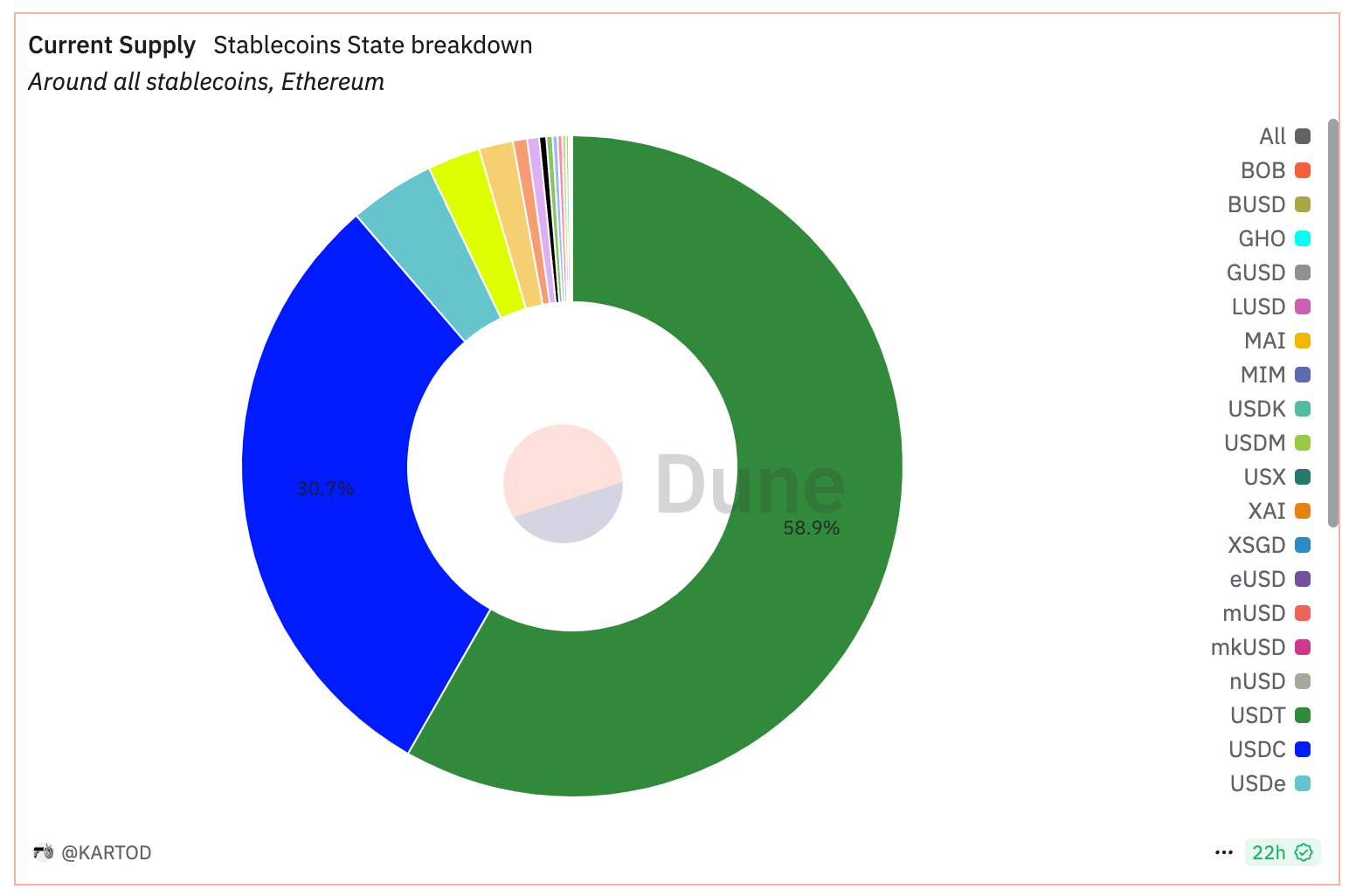

For years, the stablecoin landscape has been dominated by two giants: Tether's USDT ($144 billion market cap) and Circle's USDC ($60 billion).

Together, they control over 85% of the market.

For traditional finance behemoths like Fidelity, stablecoins represent both opportunity and necessity.

With $5.9 trillion under management, Fidelity's reported stablecoin development is part of a broader strategy to expand into the tokenised bond market, where BlackRock and Franklin Templeton have already accumulated over $2 billion.

Bank of America's CEO has openly stated the firm would launch a stablecoin once legislation passes. BlackRock and Franklin Templeton already offer tokenised money market funds with over $2 billion in combined assets.

"As soon as this legislation passes, there are going to be 10,000 companies looking at this," predicted Niklas Kunkel, founder of blockchain oracle builder Chronicle Labs.

This isn't hyperbole. The modern financial system already contains multiple representations of the dollar – bank deposits, money market funds, commercial paper, certificates of deposit. Stablecoins simply digitise and make these representations programmable and instantly transferable.

In this new landscape, differentiation becomes critical.

We're already seeing this play out in real time.

Yield competition: Newer entrants like Noble's USDN and Usual's USD0 pass through Treasury bill yields to users. Even Coinbase now offers 4.1% on USDC holdings. World Liberty's USD1, notably, offers no yield – perhaps to avoid securities classification.

Trust and backing: Custodia CEO Caitlin Long emphasises her stablecoin represents "real dollars" versus "synthetic dollars". Wyoming's stablecoin will maintain 102% capitalisation backed by cash, US Treasury bonds and repurchase agreements.

Distribution strategies: World Liberty Financial will likely "rely on deals to seed deposits for USD1," according to Blockworks' Luke Leasure, potentially including "yield pass packs to depositors" or exchanging WLFI tokens.

Technical differentiation: Fidelity is testing its stablecoin as part of a broader push into tokenisation, including an Ethereum-based "OnChain" share class for its US dollar money market fund. Wyoming has selected LayerZero for interoperability across potentially nine blockchains, including Ethereum and Solana.

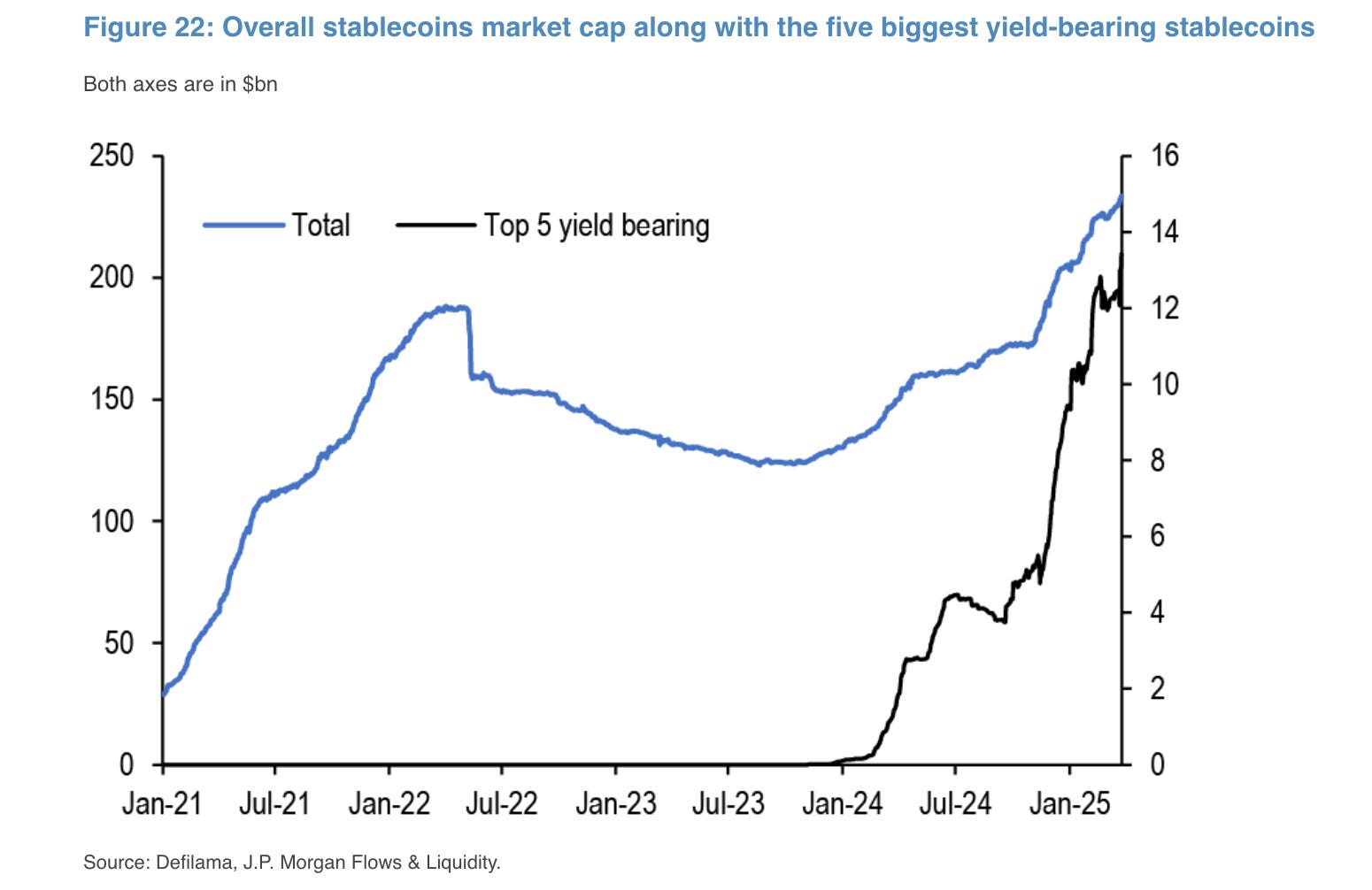

JPMorgan analysts predict that yield-bearing stablecoins — currently just 6% of the stablecoin market — could potentially capture up to 50% of the total market cap in the coming years.

The top five yield-bearing stablecoins (Ethena's USDe, Sky Dollar's USDS, BlackRock's BUIDL, Usual Protocol's USD0 and Ondo Finance's USDY) have already experienced explosive growth since the US election, expanding from around $4 billion to over $13 billion in combined market cap.

For financial institutions, stablecoins offer an unprecedented opportunity to transform payments from a cost centre into a profit engine. By holding customer deposits in low-risk yield-generating assets like treasuries, they can directly capture the interest—just as Tether did when it earned $13 billion last year, while Circle raked in $825 million in just six months.

They can also drastically cut costs by eliminating intermediaries like Visa and Mastercard, which typically consume 1.6-3% per transaction. A native stablecoin could settle payments at nearly zero cost, boosting margins and enabling cheaper payment solutions.

Wall Street's approach is clear: adopt blockchain technology while maintaining centralised control over issuance, compliance, and governance. Use new technology to preserve existing power structures—and their profits.

Wyoming Stakes its Sovereignty

In America's least populated state, a radically different vision is taking shape.

At the DC Blockchain Summit, Wyoming Governor Mark Gordon announced that the state has selected interoperability protocol LayerZero as its partner for launching WYST, their state-issued stablecoin, potentially as soon as July.

Wyoming's token will be backed by cash, US Treasury bonds, and repurchase agreements, with a statutory requirement of 102% capitalisation. Interest earned would fund state priorities like education and infrastructure.

What's truly revolutionary is Wyoming's plan to issue this stablecoin on permissionless networks. The state is currently testing it on multiple blockchains, including Avalanche, Solana, and Ethereum.

This represents a fundamentally different philosophy about what money should be in the digital age. While Wall Street aims to maintain centralised control, Wyoming is embracing the open, permissionless ethos of crypto-native finance.

Wyoming's approach reflects the idea that innovation comes from the periphery rather than the centre. Their stablecoin is essentially a bid for financial sovereignty and a challenge to federal monetary monopoly.

The Trump Connection and Political Backlash

Adding an unprecedented political dimension to this collision is World Liberty Financial's USD1 stablecoin, backed by the Trump family, which launched on March 25.

The Trump connection hasn't gone unnoticed. On March 28, five Democratic senators, led by Elizabeth Warren, sent letters to Federal Reserve and OCC leadership questioning the "unprecedented risks" of having a sitting president overseeing a stablecoin from which he could personally profit.

"President Trump's involvement in this venture, as he strips financial regulators of their independence and Congress simultaneously considers stablecoin legislation, presents an extraordinary conflict of interest that could create unprecedented risks to our financial system," the senators wrote.

Warren went further on social media, calling the project a "grift" to "enrich" Trump and warning that Congress should "fix the current stablecoin bill moving through the Senate that will make it easier for Trump — and Elon Musk — to take control of your money."

This political dimension shouldn't be underestimated. "We are going to keep the US the dominant reserve currency in the world, and we're going to use stablecoins to do that," Treasury Secretary Scott Bessent said at the White House Crypto Summit.

The stablecoin race has become explicitly tied to American economic nationalism—and now embroiled in partisan conflict.

The Regulatory Battleground

These competing visions are colliding in the regulatory arena, where the stakes couldn't be higher.

The US House of Representatives recently released the text of its STABLE Act, while the Senate Banking Committee has already advanced its GENIUS Act. Rep. Bryan Steil, who leads the House Financial Services Committee's crypto panel, says the two bills are "roughly 80% similar" with lawmakers working to close that gap.

Read: How STABLE is the GENIUS Act? ⚖️

French Hill, Chair of the House Financial Services Committee, has also indicated that a revised draft of the comprehensive market structure bill (known as FIT21) would be published in the "next few days."

Bo Hines, executive director of the Presidential Council of Advisers for Digital Assets, indicated that stablecoin legislation could be on the president's desk within two months.

Not everyone supports this regulatory momentum. Senator Kirsten Gillibrand warned about the potential systemic risks of yield-bearing stablecoins at the DC Blockchain Summit:

"If they are issuing interest, there is no reason to put your money in a local bank. If there is no reason to put your money in a local bank, who is going to give you a mortgage? If there is no deposit, small banks cannot do that anymore; it will collapse the financial services system that people rely on."

JPMorgan notes that traditional stablecoins like USDT and USDC don't share reserve yields with users because doing so would classify them as securities, imposing additional compliance requirements. This creates a distinction between securities-classified yield-bearing stablecoins and payment-focused non-yield types.

The Dollar Dominance Question

This stablecoin collision is occurring against the backdrop of a shifting global financial order. The dollar remains the world's reserve currency, but its dominance has been gradually eroding.

The stablecoin race can be seen as a defensive move — an attempt to modernise the dollar's infrastructure to preserve its central role in global trade and finance.

As Austin Campbell noted at the Digital Asset Summit, "If we think about marginal buyers of US debt, a lot of foreign governments have been reducing their holdings of treasuries. And the great irony…[and] countervailing weight is that the people in those countries are increasing their holdings of US Treasuries through stablecoins."

This suggests stablecoins might actually be reinforcing dollar dominance from the bottom up, even as some governments move away from it at the top.

Alex Thorn, head of firmwide research at Galaxy Digital, made an even more striking claim: "Stablecoins are seen as more politically easy to do in Congress but actually will be dramatically more impactful to the United States and the world than market structure [legislation]... the stablecoin bill could solidify dollar dominance for 100 years."

Token Dispatch View 🔍

There's a paradox here: by creating dozens or potentially hundreds of different "digital dollars," each with its own governance model, technical features, and regulatory status, is the United States actually fragmenting rather than reinforcing the dollar's strength?

A single, unified dollar has been one of America's greatest economic advantages. A fragmented landscape of competing stablecoins might inadvertently undermine that unity, even as each individual issuer tries to promote it.

As these distinct approaches proliferate, collisions are inevitable on multiple fronts.

First, the yield battleground. Tokenised Treasuries and yield-bearing stablecoins are growing rapidly, offering interest without requiring holders to engage in risky trading or lending activities. Major crypto trading platforms like Deribit and FalconX now accept them as collateral, enabling traders to earn yield on posted margin.

Second, the liquidity challenge. Despite rapid growth, yield-bearing stablecoins face a significant liquidity disadvantage against established players like Tether's USDT. With a combined market cap of around $230 billion across multiple blockchains and centralised exchanges, traditional stablecoins offer efficient, fast, and low-cost transactions even at large volumes.

Third, the regulatory collision. Will stablecoins be regulated primarily as banks, as securities, or through a new framework entirely? The answer will determine which faction has the advantage. JPMorgan analysts noted that the SEC's recent approval of Figure Markets' application for a yield-bearing stablecoin, YLDS, which is registered as a security, provides momentum to this segment but also establishes a separate regulatory track.

Fourth, the market differentiation problem. What will set one USD-pegged token apart from another in a landscape potentially featuring hundreds? According to Austin Campbell of Hilltop DAO, the narrative around stablecoins is often overcomplicated: "Generally, people overcomplicate the discussion around stablecoins, and also call a lot of things 'stablecoins' that shouldn't be called stablecoins. But a properly constructed stablecoin is just a box that basically holds stuff that looks like T-bills and treasuries. Very simple. And it's just represented on a blockchain."

Finally, the global competition. Countries like Japan are entering the stablecoin market, with Circle securing a license to operate USDC there in partnership with SBI Holdings. This international dimension adds another layer of complexity to an already crowded field.

Week That Was 📆

Saturday: Crypto, Trump, and the Conflict💸

Thursday: Can GameStop’s BTC Bet Save the Day? 🎮

Wednesday: The Curious Case of Kraken 🦑

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. You can find all about us here 🙌

If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us.

Disclaimer: This newsletter contains sponsored content and affiliate links. All sponsored content is clearly marked. Opinions expressed by sponsors or in sponsored content are their own and do not necessarily reflect the views of this newsletter or its authors. We may receive compensation from featured products/services. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.